Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

A recent executive order may pave the way for alternative investments (like private equity, real estate, and cryptocurrency) inside 401(k) and other employer retirement plans. While this could open up trillions of dollars in new investment opportunities, it also raises questions about risk, fiduciary responsibility, and whether these options truly belong in most investors’ portfolios. We break down the proposed changes, explain how they might impact your retirement plan, and share how to stay focused on a proven wealth-building path without chasing the “hot dot.”

Then we answer your financial questions on topics like entrepreneurship, high-interest debt, rental properties, and a whole lot more!

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Brian: Big changes potentially coming to your 401(k). We just want to load you up. What do you actually need to know?

Bo: And Brian, I am so excited about this because we know that for most people, their 401(k) is one of the single most valuable tools that they have in their wealth building toolkit. And a lot of millionaires, their 401(k) is the first account to actually cross into the two comma club. So, whenever there are changes or whenever there are things that happen that may impact your retirement account, we want to make sure that you know about them. And that’s exactly what we’re going to go over today.

Brian: Well, I believe this was last Thursday. I didn’t have this on my bingo card for the day, but my feed started showing up, all of a sudden there an executive order had been issued on 401(k)s. And here’s actually we did a screenshot, “Democratizing Access to Alternative Assets for 401(k) Investors,” signed in on August 7th. So, as you guys know, we try not to do politics, but it’s one of those things where we have to make sure because one of your biggest assets is going to be your 401(k). As Bo’s shared, it’s the first account for most millionaires that crosses into that seven figure status. So, we just kind of wanted to look and say, hey, is there anything to this? What do you actually need to know? And will this actually impact your 401(k)?

Bo: So, let me walk through what the executive order says and then Brian, I want you to explain exactly what that means sort of in layman terms because this is what it said. The Secretary of Labor shall re-examine guidance on fiduciary duties on asset allocation under ERISA. For those that don’t know, ERISA is just the governing body that oversees employer sponsored retirement plans. Think 401(k), 403(b), and so on. They shall clarify rules and guidelines around alternative asset classes under plans that fall under this subsection and these alternative assets are defined as private equity, cryptocurrencies, real estate and a number of others. And the SEC shall consider ways to facilitate access to these investments inside of 401(k)s, inside of 403(b)s and other types of accounts. That’s what the executive order says. Brian, what on earth does this mean?

Brian: Well, I think what they’re trying to do is add more assets or investment choices to 401(k)s, but these are typically, private equity, cryptocurrency, real estate. A lot of these things were what required accredited investors in the past. So, it’s interesting to see and that’s what we have a few more slides that we’ll cover, but my big takeaway is that anybody who’s ever set up a 401(k) is that there’s a fiduciary standard that goes into designing a 401(k). So, as a trustee, and Bo and I are trustees of our current 401(k), you always get nervous because the attorneys will scare you to death on what are your risks as the trustee for this plan. So, I think that this is just one of those things where they’re trying to add more asset opportunities or investment opportunities into 401(k)s, but I’ll be curious to see how this actually plays out. And that probably is a good segue into the next thing because what this means is they have like 180 days for them to give a report on what’s the viability of adding these additional asset classes to 401(k)s.

Bo: Yeah. It’ll clear the path for the 401(k) fiduciaries to decide how they’re going to do this, how they’re going to roll it up. And if it happens, this potentially could open up $12 trillion in retirement assets or about 20% of the overall market to invest in these types of asset classes. Again, most folks, their 401(k) is the largest investment account that they have, the largest pot of money they have access to. And so now they are saying, “Hey, we want this pot of money, these pot of assets to be able to invest in even more things and even different things.” And you know, you might be thinking, “Oh, this is a good thing. More options is better. When I go to the buffet, I want as many options there as possible.” But Brian, I don’t know if I’m going to sign off that I’m super excited about this.

Brian: Yeah. Let’s kind of go ahead and pivot to what does this actually mean for you first? I want to make sure everybody, and I’m going to get to that part of it, but I think I want everybody to take a deep breath. Your current regular investments, they’re not going away. That’s right. But I do think that you make a good point, Bo. I mean, we’ve done a lot of 401(k) implementations and sometimes you’ll see a plan that will offer 120 options. You know, they’ll give you every asset class. They’ll give you all the different versions of it. And when we’ve set up 401(k)s with employers, we often try to say, “Hey, let’s dial this down to 12 to 14 investments.” So we can get the different asset classes, but let’s not overwhelm the investors because we need to get the core investments in there. And that’s the key part. I don’t want this to dissuade people from making those basic, getting the S&P, getting the market instead of trying to get into these fancier, more sophisticated investments way ahead of when they need to. And that’s kind of the big takeaway is that I don’t want people to get distracted by chasing the hot dot, but we’ll keep going.

Bo: Yeah. And just to kind of make sure that you’re aware, even if this ends up moving forward, it doesn’t mean that it’s going to exactly happen inside your 401(k). What will likely happen is they will expand the ability for these things to be in 401(k)s. It’ll be up for the individual fiduciaries to decide if that goes in. And a lot of fiduciaries are still going to be concerned about whether or not making that available inside of the retirement account is them still satisfying their fiduciary duty. So even if this is allowed in some 401(k) plans or some 403(b) plans, it does not mean that it’s going to be available in yours. And even if it happens, it likely means that it’s not going to happen immediately. There’s still going to be some lag time before this gets implemented. Again, there’s a lot of unknown unknowns around this. What will most likely happen is that 401(k)s will begin to offer some sort of like self-directed brokerage option and then it’s inside of that self-directed brokerage option you’ll be able to do these alternative investments but it’s not going to move quickly. Remember this is like 20% of the overall market that is represented by retirement plan assets. So this is not, I do not think it’s going to move super quickly.

Brian: So let’s actually, this is the part I want to get to, key takeaways for you. We have done Making a Millionaire where I pick on some of our guests because I feel like they get easily distracted by things that have come their way and I think that this is the risk that a lot of Americans will fall into if you’re not careful. First of all, we have to get over the boundary of will fiduciaries even take this risk since their rear ends are kind of on the line unless they somehow change the rules where the fiduciary standard is lowered significantly on these plans. And then it’s back to the point of a lot of what you’re trying to do with your retirement plan. If you pull up the FOO, your key investments when you get to five and six, we want you just buying into the market and it’s going to be hard to do better than just core index funds or index target retirement funds. All the asset classes that were listed on this executive order are items I would consider to be step eight. And since unfortunately the majority, vast majority of Americans, there’s even a stat that I saw that was close to half of Americans don’t even know what’s in their 401(k). So I mean the fact is don’t get distracted chasing the hot dot. Majority of people still need to stay in that level of just do those core investments, the index funds and so forth. And then of course I think if you’re higher up on the net worth scale, you’ve got the good foundation underneath you. Yeah, this might create some opportunity as a step eight, but for the vast majority, I hope it doesn’t create a distraction.

Bo: Well, and you sort of alluded to this, more options does not mean better options. And one thing that we want to make sure you’re aware of is that higher risk does not always guarantee higher returns. We always think about things in terms of the risk spectrum. If I do something more aggressive and I take more risk then that means I will get a higher rate of return. That’s the wrong mindset. The mindset should be if I am willing to take more risk then I should be given a higher rate of return for the risk I’m taking. And if that does not exist perhaps that’s not something that I should pursue. So, a lot of these private placement, private equity, real estate, even some of the crypto investments may be far out on the risk scale, but that does not necessarily correlate to meaning that you’re going to have higher returns. And I’m worried that a lot of folks who should be focusing on steps one through seven will likely get distracted because they forget that building wealth, it is not necessarily easy, but it is remarkably simple.

Brian: It’s simple, but it’s hard because people get distracted. They fall into these traps. I still stand by the fact that I think about every year when I renew my errors and omissions insurance for our wealth management firm. One of the first questions they ask me is how many private placements are you putting clients in because these are higher risk type of investments. So, it offers a higher exposure to your insurance companies since you’re on the line with this fiduciary standard. So just me knowing the experience of doing the application process every year when I’m renewing my insurance. I just don’t know that this is probably going to turn out to be much ado about nothing. I do think, we were talking about just internally. This is how nerdy we are. We actually talk about this stuff is that I think that if you run a hedge fund, if you run a private equity company, that’s probably where some of this pressure is coming from. They’re going to self-deal and probably add this stuff. They’ll be willing to take the risk because it opens up so much in access to assets. And I do think and this kind of surprised me. I felt like the old man at the table when we were talking about, everybody on the content team said that probably where you’ll first see this is crypto will probably make it into, I think that’s the one that will be the most likely to be most highly utilized would be my guess. So in the comments, feel free or in the chat, you know, give us your opinions because this is still a lot of area that will be uncovered over the next 180 days, but we just want to make sure in typical Money Guy fashion, we load you up. But it is one of those things and I think this is probably the last key takeaway is remember you want to have a plan that’s good before that no matter what comes your way that even if you’re in the middle of chaos it’s good during and then it’s good after and represents the intersection of you know what are your goals, what are you trying to accomplish. Don’t put on your blinders and stick with the plan that’s going to get you there. Don’t get distracted by chasing the hot dot of what is the latest greatest trend that’s making it through the news cycle.

Bo: I love, Brian, that we get to sit in this spot, that we get to see this information that comes out and hopefully help you discern and figure out, okay, is this important to me? How does this affect me? And what are the things that I should watch out for? We love that we get to be here in this place doing that. We also love that while we’re here, every Tuesday morning at 10 a.m. Central, we can load you up with information. We can answer your questions. So right now, if you have a question you want to get our take, you want us to weigh in on, we have the team out in the wings collecting your questions. Make sure that you get them in the chat because we truly do believe that there is a better way to do money. So with that, creative director Rebie, I’m going to throw it over to you.

Rebie: I have a question from Manta Galaxy to kick us off. It says, “I’m trying not to be FOO-ish. My wife and I in our 30s have 5.5 months in our emergency fund. Should we start transitioning to step five now and maximize time in the market or should we reach our goal of six months first?”

Brian: Well, there’s a lot of context missing in that question.

Bo: Yeah, I would say the answer is it depends, but we can navigate through this. First I do think it’s important to note that as we design the financial order of operations, Brian, you hold the thing up. It’s supposed to be a nine-step process that helps you figure out what you do with your next dollar. And the mindset we want you to have is I complete one step before I move on to the next one. So, I want to make sure that I have my deductibles covered and then once I’ve done that, then I can go get my employer match. I want to get all my employer match. And once I’ve done that, then I can go pay off my high-interest debt. And then once I paid off my high interest debt, I can go build up my emergency fund. And then once I have a fully funded emergency fund, I can then go to step five. I can then go to my Roth and HSA. But fully funded emergency fund is is a little bit subjective because who gets to define what your emergency fund should be? You get to define that. Now, our general guidance is that it should be somewhere for most people in the accumulation phase between 3 months of living expenses and 6 months of living expenses. And there are a number of variables that will impact and dictate that. But you need to decide for you, okay, are we a two-income household? If we were to lose our job, how likely would we replace it? What’s our other investment accounts look like? What sort of safety nets or backdrops do we have in place to define what your emergency fund should be? And you may arrive at the conclusion, hey, you know what, five and a half months is a fully funded emergency fund. Or you may say, hey, it’s not quite there. So the answer of whether or not you can move forward, I think depends on how you define fully funded.

Brian: Let’s put some meat on those bones. And the fact that let’s just say Manta Galaxy, both spouses are working, both make a great living, both of them are in high demand careers where they could easily replace their jobs if one of them got laid off. That is going to probably be somebody who’s closer to a three-month cash reserves than a six months. And maybe they’re at five and a half months just because of a personal preference or risk averse, you know, where they just are averse to taking on additional risk. That is, I’m going to tell you there’s nothing wrong with you transitioning on over to step five because you probably have put in the work, you’ve risk assessed it, and you’re there. Now, we could flip the coin and say, what happens if Manta Galaxy, only one spouse is working and they’re in a more specialized career field where yeah, if they got laid off, it’s going to create a lot of hardship for the family that you definitely need to be at 6 months. If you resemble that structure and yes, it is very FOO-ish. If you are at five and a half months and you haven’t just finished the drill and loaded up, and the reason we’re so strict about this and why we call it FOO-ish, which is very FOO-ish, is because you can actually put your financial life in the ditch if you run out of cash. We all take cash for granted just like we do the oxygen we breathe until we go underwater and then we realize, oh my goodness, there’s a reason that we need to make sure we keep an emergency reserve so we don’t make those desperate decisions that allow us to go into debt or just make crazy decisions that are less than ideal for our future selves.

Rebie: Love it. Well, Manta Galaxy, thank you for being here and for asking the question. Hope that helps you think it through.

Brian: I have to ask now because when I see something like Manta Galaxy, was that also a meme that me and Bo missed from the early 2000s that just completely occupied the comment section?

Rebie: Don’t recognize this one. But of course, I kind of missed the last one, too.

Brian: Trogdor, you shouldn’t try that because now we just, all you do is reignite that people are going to be like, “I knew these guys weren’t that cool.”

Bo: I don’t think that’s the conclusion that they arrived at.

Rebie:I don’t know. What conclusion do you arrive to? Let us know. Because we didn’t know who Trogdor was.

Bo: We do now though. Burn the roofs. Thatch the roofs. Was that what they were saying? What the comments were saying? Burn the thatched roof. Oh gosh. It was a thing. I saw it in the comments.

Rebie: All right, we’re gonna, sorry, I shouldn’t have gone for that. That’s on me. I’ll take the blame for that. Okay. Thank you, Brian, for falling on the sword.

Rebie: Paul T thankfully has a question up next. He says, “My wife and I together have about $22K in old 401(k)s that we want to convert to IRA. Should we roll them into rollover IRAs or pay the fees to convert them into Roth IRAs?” I have one and she doesn’t. I think he means Roth IRAs.

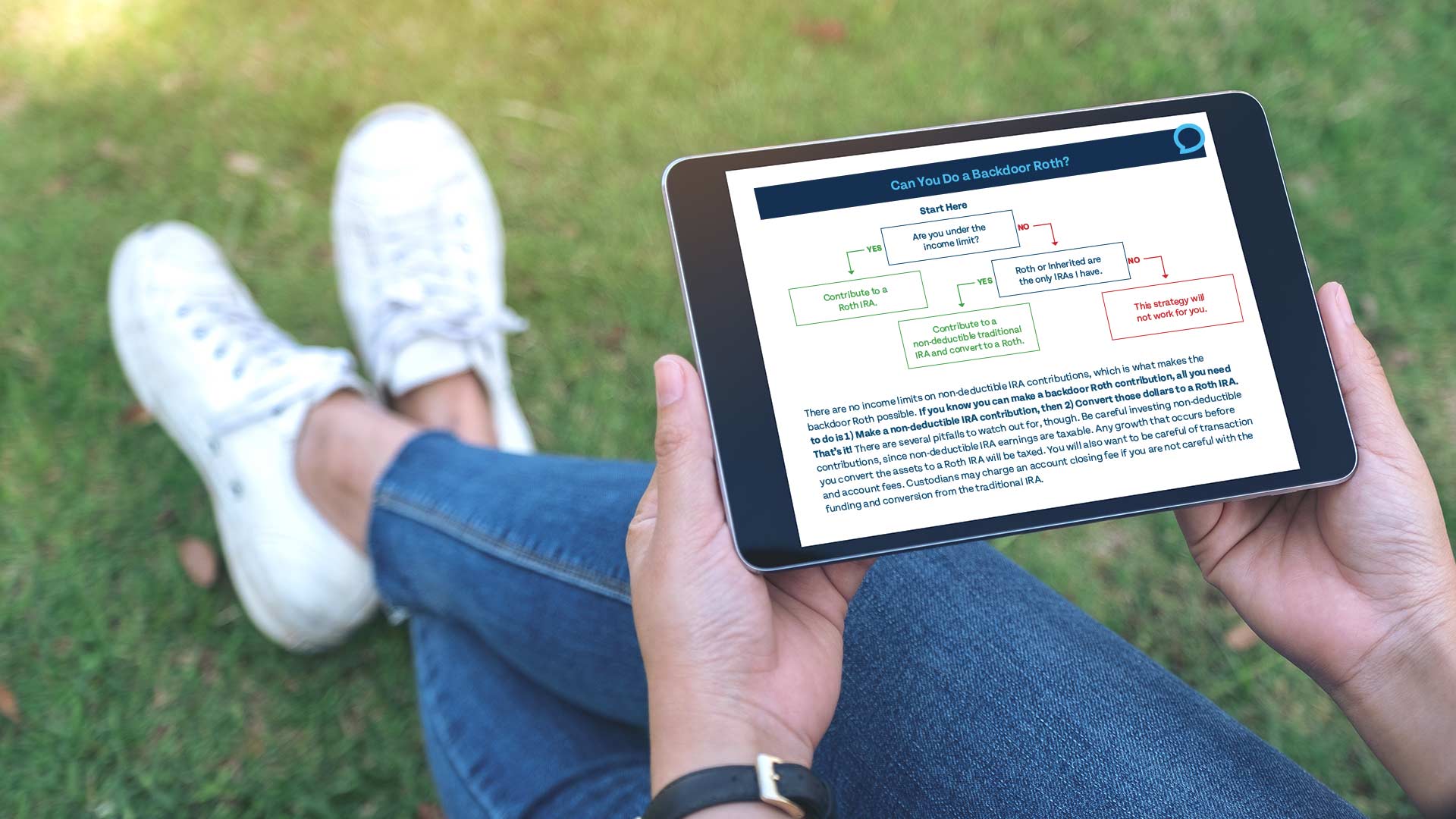

Bo: Oh. Well, it’s not uncommon for someone to find themselves, Paul, in the situation where they have like a patchwork quilt of former employers. I worked at this job and I contributed to the 401(k) and then I left it and then I got another job and I left it and all of a sudden you look back and you have this trail of old employer sponsored plans that you think, man, wouldn’t it be nice if I did something with those? And what a lot of people don’t realize is that when you leave an employer, you really have four options of what to do with that old 401(k). And I say four, but it’s really only three because you never do this one. This fourth one is to cash it out. And that’s what I think a lot of people do, but that’s like the absolute worst thing because if you’re under 59 and a half and you cash it out, you’re going to pay ordinary income taxes as well as a penalty on that to pull that money out. So that one doesn’t make sense. So then you really have three options. Option number one, leave it where it is. Option number two, roll it into your new employer sponsored plan, whether it be a 401(k) or 403(b) or something like that. Or option number three, you can roll it into an IRA. And then this is exactly Paul’s question. By the way, if you’re curious about what to do with an old retirement plan, I think we have a resource at moneyguy.com/resources and it’s called Got an Old 401(k)? So, if you want to know like what’s the flowchart, how do I think through that? Go check that out at moneyguy.com/resources. But Paul sounds like he’s decided he wants to do this first. So, I’m going to roll it to an IRA. The question then becomes, what kind of IRA? And then, what should I think through as I decide?

Brian: Well, several things popped in my mind immediately is when I hear people talking about doing a Roth conversion because that’s going to create some potential taxes. So, the question I’d first have is should we go ahead and create the taxes to do the Roth conversion, or should we make sure are you maximizing steps five and six because those don’t cost any taxes if you’re loading up your annual contributions. And the reason I say is because you told us it’s $22,000 between you and your spouse’s old 401(k)s. Well, that’s less than the 401(k) contribution and that’s, you know, only a little bit over what two fully funded Roth IRAs would be. So you just got some meat on the bone and the fact that you could actually fund some of this without creating the taxes by just making sure you’re working within the financial order of operations. Now, if you’ve blown through five and six and yes, you look at this and you’re like, “Yeah, you know, this is one of those moments where my tax rates are going to spike up in the next year or two and I’d really like to clear this out because it’s going to open it up for me to do backdoor Roth contributions.” There’s a lot of things that could come into play that say, “Yeah, let’s do a Roth conversion.” But before you do that, a lot of times, especially if you work for like a Fortune 500 company or an employer that has a great 401(k), the easy answer is roll it into that new 401(k) that gets you the ERISA protection. It also allows you to do the backdoor Roth conversion strategies. There’s just a lot of benefits out there, but it is definitely one of those things you want to measure twice, cut once because there’s ramifications for whatever path you go with it. That’s why that deliverable is so powerful is because it kind of walks you through some of the decision matrix of how you decide this in a good way.

Bo: And I just want to clear up one thing in your question, Paul. I think the language you use is, “Hey, should I just pay the fees?” For most folks when they convert or when they transfer assets from one custodian to another, convert from one type of account to another, there aren’t really fees associated with it. Most of them don’t have any sort of associated charges. It’s like you think about like closing costs on a mortgage or something like that, but there are taxes due. So, what you’re really making is a tax decision, not a fee decision. If your custodian is charging you fees for moving your money, that should be a red flag anyway.

Brian: And everything we were talking about with moving it to your new employer, that’s what’s called a trustee to trustee transfer, which that rollover should be a tax-free transaction.

Rebie: That’s great, Paul T. Thank you for the question and thank you for being here on our live stream.

Rebie: Matthew T has a question for you. It says, “I am 27 with a student loan which will mature when I am 32. The interest rate is 5.375%. Do I treat this debt as step nine until I turn 30, then stop Roth contributions to prioritize it as step three, which is high interest debt?” What do you think?

Brian: This is somebody, Matthew knows our system pretty good here.

Bo: Well, so we actually have we have some rules around this, right? Because as you’re, Brian, will you hold the thing up for me? As you’re walking through the financial order of operations, one thing that you have to decide is what qualifies as high-interest debt in step three versus what qualifies as low interest debt in step nine. And what I think a lot of people might not recognize is that it changes. What may be high-interest debt to me may not be the same thing that’s high-interest debt to Brian based on my unique circumstances. And student loans is one of those where what qualifies in our opinion as high interest versus low interest changes as you age. And now we’ve got some like thoughts around this considering like you know equity risk premium and opportunity cost of your dollars. But generally speaking, Brian, where I’m going with this is our guidance is if you’re in your 20s and your student loans are below 6%, I would argue that does not count as high-interest debt in step three.

Brian: Agree, disagree, it’s built into kind of our deliverables on the site. And that’s why, but that’s why I can tell that Matthew is a true financial mutant because he’s already picked up on that when he transitions into his 30s though, there’s a step down on that interest rate. It goes from 6% down to 5%. So, I do think that Matthew, you’re spot on in the fact that look, you’ve already got some pressure building in the background also in the fact that these things will come due, you know, at 32. Yep. So, I mean, you might be at the intersection where when you cross into your 30s that you’re already going to have the pressure because you know that you’ve only got two years plus now the fact that we’d probably classify this as high interest debt. I think I would probably get very serious as you cross into your 30s. Hopefully, you have enough career traction that you’re going to have the cash flow flowing in that you’re like, “This is yeah, this is the time to get serious and let’s start tackling this.”

Rebie: Love it. Awesome. Matthew T, thank you for being here and thank you for asking the question.

Bo: One thing, can I just tell Matthew T to go do one more thing? He’s already done this obviously, but you should go to moneyguy.com/resources, play with some of our calculators. You can look at the compound interest calculator or what I want you to play with specifically is the wealth multiplier calculator because what I want you to see is that money in from age 27 to 29. I just want you to go look at what those wealth multipliers are at those ages. And yeah, while you could go satisfy this 5.375% interest, if you took those dollars and you applied that wealth multiplier to them to let them grow from now until 65, it gets really, really, really, really exciting for the dollars that you can save in these next three years.

Rebie: Yeah. Well said. Moneyguy.com/resources. Click on our wealth multiplier calculator.

Brian: I’m wasting sticky notes. This one was still good. I got more meat on this one. It’s almost like they make technology to where you can write notes.

Bo: It’s so funny because I don’t know if you guys have checked this out. We do this show every other Monday called Making a Millionaire where you can go watch us do a deep dive with folks that are either millionaires or millionaires in the making. It’s a lot of fun. Both of us use Remarkables in the show. I never bring it over to this set because I got a computer here and I feel like I’d have too many things going on. You look, a Remarkable, an iPhone and a laptop. It’d be something. It’d be something. So that’s why I stick with the old sticky notes for my notes.

Rebie: Interesting. We just need a bigger desk. Maybe that’s it.

Rebie: All right. Sneed has a question for you. “I have a $25K capital loss on a property and I’m just below the 15% gains or 22% tax bracket. Would you hold on to the losses for later pay raises or take $3K deductions even at a low tax bracket?”

Brian: Okay, so fancy tax question for you. Just below the 15%, 22% bracket, would you hold on the losses for later? This is one of those things. Look, I like being tax smart, but it’s also when you’re doing year-end planning, if you have the ability to rebalance and reallocate because it’s just also the better thing to do for your portfolio. This is a tool that you, I don’t know that I’m holding on to losses because of my tax rates. It comes into play. Don’t get me wrong. I’m not saying, but I’m thinking more if you got the intersection of portfolio management plus tax policy. I think the portfolio management is a bigger determining factor than transitioning from 15 to 22%.

Bo: Yeah. I think, and also capital gains. I mean because that 22% is a marginal rate. 15% is, you’re going where I was going. You said, “Okay, I’ve got these losses.” And generally speaking, the way that capital losses work is you can use capital losses to offset capital gains. So, they can net to zero in any given year. Well, if you’re below the 15% capital gains bracket, and you’re in the 0% capital gains, you’re thinking, “Okay, well, if I just take capital gains, I’m going to pay 0% on that. So, it’s not really valuable for me to then use losses and offset money that wouldn’t be taxed anyways.” And I tend to agree with that. However, there is also this idea that if you have all of your capital losses and they offset all of your capital gains and you have even more than the capital gains you generated, you can actually then use up to $3,000 to offset your ordinary income. Well, now we’re talking about, okay, now it’s some meaningful tax savings. If I’m in the 22% marginal tax bracket federally and I can use $3,000 of those losses to offset that, well then there is some value in doing that. So, it’s difficult to give you like specific guidance not knowing what the rest of your tax return looks like. But it is one of those things you want to think about because a lot of folks get so caught up and I want to pay as little tax today as I can. I want to get today’s taxes as low as low as low as low as low. What we think about makes a lot more sense and this is what we want financial mutants focusing on is we want you to think about how much am I going to pay in taxes over my lifetime, like what’s my lifetime tax bill going to be because so often we will see people capitalize on strategies today to drive their taxes as low as possible and then what happens we get in the future and all that planning they did is unwound because they didn’t think two or three steps ahead. Here’s a really easy example of someone who does this. A lot of Fortune 100 companies will offer what’s called deferred compensation plans where you can say, “Hey, instead of paying me my salary, I want to defer my income into the future.” And so you think, “Oh, that’s great. I’m going to really drop my income, I’m going to defer. I’m not going to get taxed on it today. I’m going to put it in this deferred comp plan. It’ll pay out later.” Well, what they don’t recognize is, man, if I do that, but I’m not strategic in thinking about how big I build that pot or how I’m going to distribute that from the time I retire until I deplete that pot. All you may have done is sacrificed paying, you know, 35%, 32% today in exchange for paying 37% in the future. You didn’t actually save yourself anything even though you thought you were going to. So thinking through it two or three steps ahead is likely going to be a valuable exercise.

Brian: What do you think about the fact, and it’s okay if you disagree with me and I’m just going to make up numbers because we don’t know, is if he’s got a $25,000 capital loss and let’s just say that this was an initial investment that he put $125,000 in, now it’s worth market value of $100,000, $25,000 loss. Do you take into account the portfolio management side of it? How many people do we see that come to us that they have these investments that you’re like there’s just zero chance that that thing is recovering? What it is worth now is where it’s going to probably be 18, 24, 36 months from now and the opportunity cost of correcting a wrong and getting to fresh green shoots always comes into play too.

Bo: Yeah. No, 100% it does. I use this analogy all the time when I’m talking to clients. If you were, say you were riding a bicycle, right? And you’re riding a bicycle down a valley. And so for those of you out there on the podcast, you know, you kind of come to the bottom of the valley and then you come back up to the top to the peak. If you were riding a bicycle and your tire got flat at the bottom of the valley, you’re not going to think to yourself, you know what? I’m going to wait till I get back up to the top and then I’m going to change this tire. No, you’re going to say, man, okay, I’m at the bottom. I’m down here. I’ve had this thing happen. Perhaps if I put a new tire on this bicycle, I might be able to get back to where I was much more quickly, much more efficiently with much less pain. Investing is no different. We see people all the time, they’ll buy this stock and oh, this is the next big stock and all of a sudden it tanks and it’s down 15, 20, 30%. Like, oh man, I’m never going to sell it. I can’t. I got to wait till it comes back. Got to wait till it comes back. There is opportunity cost in waiting till something comes back. So, you want to make sure you think through that. So I think absolutely portfolio allocation and capital usage certainly comes into play.

Brian: Well, and how many times have we heard people say, “I haven’t lost anything until I sell it.” Yeah. And we’re like, “Well, you know, you have to still handicap if this thing’s ever coming back.” If you own Blockbuster stock, you know, it’s probably not coming back.

Bo: What’s that? Because there’s a funny skit. Man, we did a, we did a react video. By the way, if you’re not subscribed, every other Monday when we’re not doing Making a Millionaires, we release these react videos. We actually just had one come out yesterday. Brooklyn 99.

Brian: Did you just call it Brooklyn? Did y’all hear Brooklyn 999? Let’s put a period between those nines. Brooklyn 99. Oh, 99. I got 99 Brooklyns.

Bo: Yeah. So, anyways, we did a react to like some very popular, there were some Office, some Schitt’s Creek, some Brooklyn 99. And that was one of them. They had Blockbuster stock certificates that were not as valuable as they once were.

Brian: Yep. Brooklyn 99 rotation in the Preston household.

Bo: That’s hilarious.

Rebie: All right. Ready for the next question? It’s from Andrew. He says, “How should someone prepare for a six-month unpaid sabbatical? What would you do? What would you tell them to do?

Bo: Well, I’m assuming, you know, the question you’re asking is, hey, for six months, I’m going to have income go away. I’m going on a sabbatical. I’m not going to have income coming in. And you got to think about, okay, well, what’s my income actually do? It allows me to pay for the expenses that I incur in life. So, it pays for rent and mortgage and utilities and groceries and all the things necessary. So, if I’m not going to have income coming in to pay my bills, the natural place that my head immediately goes anytime I’m planning for some sort of period without income, I think that cash is probably your friend. And you want to build up an emergency fund above and beyond. And I wouldn’t even call it an emergency fund. I’d call this like a sabbatical fund to make sure that you can cover that six months of living expenses plus maybe even a few more if it’s not guaranteed you’re going to be able to come back to work.

Brian: Yeah. I mean, look, this is all about preparation and planning is that you plan accordingly if you take advantage of this sabbatical is that you’ve measured twice, cut once, that you have enough cash to pay all the bills and do the things. And then the second thing is more philosophical is if you’re going to do this six months, let’s make it purposeful because that’s what when you do these type of things, it’s supposed to kind of be a regenerative that you come out even better on the other side of it. So let’s be purposeful with how you spend that six months and that’s going to require planning and preparation as well. So I look at this as both looking at the financial side, but as well as hitting the ground running on what you’re hoping to get out of the sabbatical.

Bo: And then the other thing that I would do going into this, and we say this whenever you make any significant life change or large type purchase or investment, we want you to put on your 3D glasses. As you prepare and move into this, I want you to think through, okay, if I take the sabbatical, what’s the dream? What’s the thing that’s going to happen during the sabbatical? And what’s the thing that’s going to happen when I return from sabbatical. Then what’s the down to earth likelihood? What’s the most probable outcome? I’m going to do this. I’m going to leave. And then what really really matters is the third one, the doo-doo plan. Because and we’ve seen this happen. What happens if you think, you know what, I’m burnt out. I’ve been just grinding, grinding, grinding, grinding. I just need a break. And maybe I’m in the technology field or I’m in some like sector that’s just been very, very stressful the past couple years. And I decide I’m going to take the sabbatical. I’m going to bow out for six months, and then, you know, I’ll get right back into it. Well, all of a sudden, month five, five and a half rolls around and you start making those phone calls to try to make sure that you have placement back into the workforce and it turns out, oh man, it’s a little bit harder to enter back in at the same place that I exited. And if that’s the case, and if that’s something that could happen for you, how are you going to plan for that? How are you going to navigate that? Not saying that you shouldn’t do the sabbatical, but you should definitely think through if that’s a likely outcome, what would you do and how will you navigate that?

Brian: Yeah, I guess this is a big consideration because when I see sabbaticals, like I know a lot of employers after you work for a number of years, they’ll give you a period. Sure. But I’ve never seen six months. So that probably is more of a self-chosen. I’m going to take six months off. And I think that’s probably a very valid concern. I would definitely put on my 3D glasses.

Rebie: Good stuff, Andrew. Thank you for asking the question. I hope that helps you think through this decision and how you might prepare.

Rebie: Next question is from Jake.

Brian: Our friend Jake, the Jake, we still got that bottle of bourbon waiting for you, Jake. Jake brought gifts to Austin and we’re still waiting to partake. So now he’s got to come to Franklin.

Rebie: I know he has to come visit. Anytime, Jake. Let us know. All right. He says, “My company just announced that they are stopping the 401(k) match.” Lame. That is lame. “Is this a red flag to start looking? What’s your insight or your take on this?”

Brian: Well, I’d want to know why. Yeah. Right. Yeah. Yep. I mean, there’s multiple reasons. It could be, look, when companies are in trouble financially, sometimes this is one of the areas where you see it. But let’s go the other side of the coin is sometimes plans will restructure because a match is a guaranteed 3%, 6%, whatever it is and they might say well you know what, this is getting to be very expensive. We’d probably be better served doing a profit sharing or something that puts a little more discretion, golden handcuffs or discretion on it too because a lot of times if you’re doing safe harbors they’re 100% vested on the day they’re funded whereas these chunks of money the employer might want to make it more of an incentive for you to stay longer. So I’d want to know the why and then what is the alternative they’re offering? Because if they offer a more lucrative profit sharing, then okay, maybe this is okay. Especially if you’ve been there for a number of years and you’re fully vested in everything, I’d be like, okay, they’re just basically restructuring how these things are. But if they’re just shutting it all down, I’d be like, what’s going on here? And sometimes now look if they were recently purchased you know and maybe it was like a private equity company bought your firm and all of a sudden they’re trying to come up with cost cutting measures, I mean then that’s just probably the new trend of your employer is going to be lean because they’re trying to restructure it in the next three to five years to get a higher multiple.

Bo: Yeah. Sometimes it can be as innocent as restructuring. Another one that we’ve seen often is someone will have a small company, small workforce, and they’ll want to be really generous to their employees. They’ll say, “Hey, we’re going to do a dollar-for-dollar match up to 5% or a dollar-for-dollar match up to 10%.” But then as the company grows and has more success, that becomes very, very expensive. And they say, you know what, instead of doing a match, it would be less expensive for us to take away the match and we’re just going to do like a safe harbor non-elective 3%. So move away from the match and it’s just going to be like some sort of minimum contribution for the overall workforce. That could be happening. It’s not a match taking place, but there’s still employer dollars flowing into the plan. But I agree with you. I’d ask the question, well if you can, you know, maybe don’t just barge into the CEO’s office and say, “Hey, what’s going on here?” But if you could ask, “Hey, just curious what the thought process is here.” And then be discerning. It’s never a bad idea to make sure that you just kind of understand what’s going on in the environment around you and make sure that you prepare and protect yourself for that.

Bo: Yeah. Yeah, that’s good thoughts. So, maybe not time to walk out the door, but definitely figure out why. But also, you know, Franklin’s wonderful this time of year and every time of year, so start looking.

Brian: It’s a little, it’s a little humid right now, though. It’s like, “Love it here.” Brian’s like, “No, I do love it here.” I think this is a, you love it here. Beautiful. It is kind of humid right now to live and raise a family, but it is quite humid right now. But I think a lot of America’s humid right now. Lots of humidity.

Rebie: All right. Next question is from JP1208. It says, “I have about $10K left in credit card debt. It’s high interest. I’ve cut it down from $30K.” Wow. Which is great. “Should I do a $10K loan or get a 0% APR credit card or is there something else he should consider?”

Brian: Yeah. I mean, I would like to know the time frame that they went from $30K to $10K. Yeah. Because it sounds like they’re already on the path of like just take no prisoners, make it happen. I’d rather you go down that path because it just seems like the relief valve of going and getting more debt or one of those 0% APR trap cards because I mean look it works if everything lines up but if anything goes wrong those things can be a mess and usually there’s some fees when you transfer to a degree too. So I would rather you just take no prisoners and go ahead and finish the drill on that $10,000. We don’t have enough context to know how hard that’s going to be from the variables that have been provided though.

Bo: Yeah. I do not love option number one, going to take a loan out to pay it off because what I’m thinking when I hear that is, oh, that’s like a home equity line. That’s a 401(k) loan. It’s something like that. I don’t love just replacing one debt with another debt. You’re not really solving any problems. You’re just kind of exacerbating an issue. And I’ll also say this, and this may be a hot take amongst our Financial Mutant community, but I’m going to go and throw it out there. I’m not a fan of like the 0% APR transfer game. Like I recognize there’s a mathematic substantiation to doing that. I’ve got this high interest. I’m going to transfer it to a zero interest card. I’m going to pay it off. But there are trip wires and there are things that can go wrong and there are things that can go bad to make that not a good thing. I agree with you. JP, you’ve already shown that you have the propensity to knock out credit card debt from $30,000 to $10,000. What I’d love to see you do is just buckle down and finish the drill. Whatever that means. Get as lean as possible. Cut your expenses down as much as possible. Throw the kitchen sink at that. I would rather see you go sell stuff like, “Oh, you know, I’ve got old stuff in my garage or I’ve got clothes I don’t wear anymore. I’m going to do consignment.” Whatever that thing is. I’m going to go figure out a way to get super super creative to knock this out. And then once I get that $10,000 balance to zero, I’m going to count all that interest that I accrued as sort of an education tax that I paid to learn what to not ever do again. And I’m going to get it down to zero. And as much as I can control it, I’m never ever ever ever going to run up credit card debt again. I’m going to start following the financial order of operations. I’m going to start building up my emergency fund. I’m going to have a fully funded emergency fund so that I have that thing that will prevent me from finding myself in this position again.

Brian: I think a lot of Americans, they see debt, specifically consumer debt and credit card debt, as the bridge to solve a big problem they have is that you can go get the things you want now even though you truly can’t afford it and then you’ll catch back up. And that’s, we know that’s a trap. It’s a bridge to nowhere. You’ve obviously been on that bridge. You’ve realized what a trap it is. Now you’re on the way back of building yourself and clawing yourself out of this hole that you’ve had. But what I worry is that we’re redoing it with the wrong thing if you go take on more debt or these 0% credit cards because they’re going to give you relief valves of, oh, I can take the pressure off of myself and maybe I can relax. Maybe I can now reward myself because I paid off $20,000 worth of credit card. No, let’s finish the drill. It’s because you haven’t finished the project and I just don’t want these things to be a distraction from the ultimate celebration is when you’re completely out of high interest debt and now you get to start, you’re on day one of your future financial success.

Rebie: Love it. Your future financial future.

Brian: Your future financial future. Come on now. I’m good at math and at podcasting. Well, as long as you have an understanding of the English language that lets you fill in the gaps.

Bo: There you go. That’s it. That’s it. It’s working for us.

Rebie: JP1208, thank you for the question.

Rebie: Next question is from James K. It says, “We have two paid off rental or real estate properties with tenants and we’re living in our third property with money owed being $350K and at a 7.25% rate. My question is, should I sell one of the properties and be debt-free?”

Brian: There’s way too many things. I need a spreadsheet. First to make a spreadsheet, guys.

Bo: I’m so sorry that I keep plugging, but I just can’t help it because it’s so on point. We have a Making a Millionaire episode coming out in the next month. We just recently recorded it and it was almost this very thing. Hey, we’ve got this rental property, but we have this other problem that we’re trying to solve, and how do we figure that out? What are the options? And we’re able to walk through, okay, here are a number of different options available to you. The answer to your question, James, unfortunately, is it depends. It depends on a number of factors in your unique personal situation to where yeah sometimes if you have a paid-off property and maybe you look at, all right I’ve done the math and I know that I could sell this property for X dollars and I know that right now I’m bringing in Y dollars of rent and when I think about okay Y dollars of rent relative to X dollars of home value is not a great yield. Like I’m not making a ton off this money so I have all this capital tied up and maybe it’s in a house that like really ran up in 2021, 2022, 2023, but there’s not a lot of juice left in there to squeeze. So, it might just grow at the pace of inflation. Yeah, it could potentially make sense to sell one of those properties and then use that to satisfy debt or build towards other financial goals. Or if they’re already paid for and they’re already cash flowing and they’re creating an income for you and they’re a diversified source of revenue for you, it might make sense to keep it. It’s not like absolute one way or the other.

Brian: Well, also, you know, because there’s so much that we don’t know. What if you have a great tenant? We all hear the brochure is you get this tenant that’s been in there for 10, 15 years. They’re basically helping you buy this house. They give no trouble. They even make improvements. I don’t know your situation because if you have one of those tenants and then you go sell this, I mean there’s a lot of questions I would have. But I also think Bo makes a great point. That’s why I made the joke that I need a spreadsheet is because there’s just too much I don’t know. What is your opportunity cost? Because everything you do financially is an incremental decision. This path will take you here, this path will take you there. And I think our jobs as financial advisors is that we help you go down those paths without officially going down those paths. We actually get to kind of spot check, do some stress testing, do some assessments of each one of those scenarios and then you come out on the other side feeling like, yes, this is the ideal path to check all the boxes and do this well because you’ve got a great opportunity here. I mean, you have two paid for homes, you’ve got tenants that sound like they’re paying their rent, not causing a lot of trouble, but yeah, now you have a mortgage that is pretty high, you know, over 7%.

Bo: And that’s the other thing is that, you know, it doesn’t mean you’re going to be stuck at 7% forever. There we go. We so often I feel like we see people do this. They come up with a permanent solution to a temporary problem. Like selling that rental property and satisfying that debt would be a permanent solution to no longer have that rental property when in reality, what if rates drop?

Brian: Well, what if you’re able to refinance that 7% rate down to like 5.5%? And I’ve got, because we know nothing. So I love just coming up with nerdy little scenarios.

******

Bo: Editing team do not clip that right there. He said we know nothing.

Brian: Well, but it’s just, I could add Jon Snow to the end of that. But if you think about the fact of like the Making a Millionaire that you’re referencing, they lived in each one of these homes. What if this individual, what if James lived in this house two years ago and it had a huge, what if that second rental property had a huge, see, that would be a cool thing, too, because what if he had a $500,000 tax-free gain that was sitting out there? That would probably push the needle a certain way. We just don’t know, James. There’s a lot, like I said, this is the beauty of being a financial adviser is that people are like, “Hey, you do index funds. What do you guys do for clients since you use index?” I’m like, do you not realize how much financial planning a good financial planner actually does on scenario planning and figuring out how you come out on the other end of the best way? I mean, I get excited thinking of all the different things, but at the end of the day, James, this is one of those situations where it depends and it’s the personal in personal finance and this might be a great place where it makes sense to take the relationship to the next level.

Bo: A lot of times when you’re navigating these things, I just don’t know what I don’t know. And I recognize that the decision I make can have huge implications and a very long tail. You’ve likely only had to make this decision one time. But if you partner with an advisory team who’s helped hundreds of people make that decision and navigate it and seen a number of different sides, it can be an incredibly valuable thing just to give you peace of mind and help you think about the parts of the equation maybe you had not thought about.

Rebie: Yeah, it’s good stuff. If that sounds like you, go to moneyguy.com, click on become a client because then you can just learn more and see if that is actually something that is going to move the needle for you and be a level up for you in this time.

Brian: And we’ll leave the porch light on for you. Absolutely.

Rebie: Dylan M is up next. He says, “Hey, Money Guy team. Currently I’m 25, living at home after graduating college at step seven. But if I were to move out, my savings rate would go below 25%. Should I wait to move until I can keep at that 25% investing rate? What do you think Dylan should do? Should he move out?”

Brian: Bo, this is life coach Bo moment.

Bo: Well, here’s the thing, Dylan. It’s hard to answer your question definitively because both could make sense. Maybe you and mom and dad have a really good thing worked out and like, hey, I’m living with you guys and there’s a benefit. I’m cutting the grass and I do the laundry or whatever. Or maybe I’m paying you rent or I’m helping offset utilities and that’s great and I have a high savings rate. Or you can move out and spread your wings and branch out and go live on your own and do your own thing. We’ve seen both of these scenarios make sense in different situations. We’ve seen situations where we said, “No, no, the kid’s got to get out of the house. You can’t be in the house. You got to get out. You got to go start. You got to be on your own.” And we’ve seen others where it’s like, “Hey, this is a great opportunity for you to really stack cash right now. While you don’t have to be out on your own, your parents aren’t providing economic outpatient care. They’re providing a very real opportunity for you to get a leg up that might not be available to other people who don’t have a similar situation.” You have to figure out in your circumstance considering that there are two parties involved. There’s the parental party and then there is the, what’s another word for child that’s not child that’s like an adult child. You’re an adult child. You want to make sure that the decision to stay or to go does not adversely affect one or the other. Meaning, you don’t want to stay in there if it’s going to be detrimental to your parents’ long-term financial viability because they’re subsidizing your lifestyle. But also, if you going out on your own is going to cause your savings rate to drop. That’s okay. Most 25 year olds aren’t able to have a 25% savings rate. That’s okay. 25% should be the thing that you’re working towards. You may not be able to start right there. And I think that’s okay.

Brian: First of all, Dylan, kudos to you because you sound like you’re gainfully employed. You’re investing this money. If since you said you spot checked it at step seven, that means you’re loading up not only the Roth IRA, but you’re also loading up and maxing out your 401(k) at the employer. That’s well done. I mean, that’s probably your parents are very proud of that as well. But I will say I was out with multiple couples and one of them was talking about their adult child. They were trying to figure out if they’re going to put a bike lock on the fridge. So you have to ask, you know, I would ask you to triage your personal situation to see are mom and dad as excited about my 25% as you are? And maybe they are. And then that’s still your best scenario to be there. But there’s also another thing that I think about, and I don’t know if this is, and you can call me an old soul for saying this. I lived with roommates until I got married. I mean, because when I was in Atlanta, I had two roommates. In college, I had multiple roommates. It’s amazing what you can afford if you can have other people’s money to bolster what you have. So I would look into that as an opportunity, too. Nothing wrong with taking on roommates. But you have to ask yourself what is my best version of myself in my 20s, best version of myself in my 30s, 40s, 50s and beyond. And there’s going to be an answer that kind of like is a shiny stone sitting in the sand that if you do the exercise, it’s going to be just you can’t avoid it and you’ll know that that’s the path you should take.

Bo: What? I’m just saying, Dylan’s like, “Nah, man. I got roommates and they’re great. They clean the house and they buy the groceries.” That’s awesome.

Brian: Now, look, y’all know, as I’ve gotten in my 50s, I’m super sentimental. I have this conflict that I want my oldest daughter as she graduates college to go be super successful, live on her own. But there’s another part of me like, man, I kind of like if you need to live at home, having her around. I mean, so you might be in a great, I mean, I think that that’s sometimes us Americans, we live in Tennessee now, and you know, we’re from Georgia. I’m jealous of people who live really close to all their relatives because there is something about and a lot of other cultures get this right with the extended families and so forth. Americans sometimes we miss on that. So is the sentimental 50-some. I’m like yeah I mean it’d be kind of nice being around the kids and the parents. So but everybody’s situation’s different. But I just want to make sure you’re living your best life and not stunning yourself by staying there too long as well.

Rebie: Some good life advice there, guys. Thank you, Dylan M, for asking the question and I hope that helps.

Rebie: Next one is from Endene. I like the question mark on that name. Was there a question at the end?

Brian: Was debating how I was going to pronounce it as I was pronouncing it. So, I’m going to go with Endene.

Rebie: Endene. Ending. The question says, “Can you apply the FOO, the financial order of operations, towards a business? I feel like we may be running a little bit too fat on cash, but we’re hesitant to take extra distributions with several more years remaining of our business loan.” What do you think? You are FOO and business guys. Yeah. What would you say to Endene?

Brian: The FOO is really a personal finance thing. I think that you are, Endene, you are running this as a CEO. You have to risk assess the situation. I’ve often said entrepreneurs have this fear. I mean, I don’t think it goes away ever completely. It hasn’t gone away yet. I mean, no, because y’all even when I paid off my mortgage, I was like, “Don’t worry, I still have plenty of debt out there.” You know, it’s one of those things where I think as a business owner and then you think about all the employees, you think about payroll. I’m always a little nervous. It’s a different mindset as a business owner than it is just for standard financial order of operations because you not only have to think about your personal finance situation, but you have to think about the viability of the business and you have to think about the viability for your employees and there’s just a lot of responsibility that’s sitting on the shoulders for business owners that I think it does make sense to have extra cash. That’s not necessarily a FOO thing. It’s more of a hey as a business I might need to keep a little more additional liquidity so that the viability of this thing can handle no matter what comes my way. I guess FOO can be modified because we say that even for retirees it goes to 18 to 24 months. I’m sorry.

Bo: No, no, no. We’re on the same page. What I would say is the FOO does not apply but the principles surrounding the FOO apply. Brian, you hold the thing up for me. You guys have probably noticed the FOO, it’s these nine steps, but they’re sort of like it’s like three steps and three steps and three steps. And I think you can approach your business stuff kind of the same way because at the top level, at the very first, you’re really focusing on like risk management. Like am I making sure that I don’t have things working against me? So like if you have super high interest debt and credit card debt inside your business, you got to knock that out. You got to get rid of that. You got to make sure that you’re not carrying that. And then you move on to like emergency reserves. Okay. Well, yeah, I do want to make sure that I keep enough in my business so that I can either pay for my outstanding business loan as that note comes due or I can satisfy payroll or I can invest in it. Those sort of things. And then once you’ve answered those, then it becomes okay, what’s the best use of capital? The best use of capital may be indeed to leave money in my business to be reinvested in my business. It’s historically why Warren Buffett says he doesn’t like to pay out dividends. Rather than me giving you the money to invest, I’m going to leave money in the entity so that we can reinvest. And I think that we can reinvest better than you can invest as a shareholder on your own. Well, you as a business owner are making that same decision when you decide, okay, do I leave money in the business to invest in the business or do I distribute it out to me? Or if you arrive at the conclusion, okay, I’ve done that and the business is great and there’s still excess capital. Okay, perhaps I do need to distribute it out to me. That would be like that bottom tranche of the financial order of operations are thinking okay how do I optimize and how do I think about that like second and third level of thinking. So I think the FOO does apply in terms of concept and philosophy, but the steps are a little bit different because businesses are very very unique and very very different in how they operate.

Brian: When I wrote Millionaire Mission, you know, because that’s really kind of the origin story of the FOO. But also at the end, the very last chapter, I talk about what I do with my own money. And one of the things I talk about in one of the closing chapters is how cash is an unbelievable wealth builder in the long term, but it’s more of a step eight of the financial order of operations. And I think for a business owner, that kind of applies to you as well. It ties into exactly what Bo was talking about is that you might need to keep a little extra powder money for opportunities as well as for being nimble in your sector or whatever your business navigates. But that’s why it’s a step eight. You know, you don’t do this until you’ve mastered steps one through seven. That’s right.

Rebie: That’s great. Well, hey, thank you. And hey, how would you say it? You want to say his name, Bo?

Bo: I do not.

Rebie: And you just didn’t put the question mark on the end. Enden or Ending, whoever you are. Thank you for the question and I hope that that helps you think about your business and the FOO in a helpful way.

Rebie: You know, if you have more questions, we have moneyguy.com/resources out there for you all the time. It’s all free resources, so be sure to go take advantage of those. We made those for you because we want it to be super accessible. Our show is super accessible. That’s why we try to be everywhere you might like to watch or listen. And that’s why we show up every Tuesday at 10:00 a.m. Central right here on YouTube answering your questions. So, be sure to check out moneyguy.com/resources and we’ll see you next Tuesday.

Brian: I thought it but I’ll say I have one closing thing is that you know we went on Iced Coffee Hour. The episode dropped on Sunday. Wowzer. Yeah. I mean, holy cow. I mean, I didn’t think that many people were interested in what we had to say, but they are and we got to talk about a lot of stuff that we don’t get to talk about here. What I thought was super fun and super interesting. So, I just got a text right before I went on recording from a childhood friend who drives, you know, works for UPS, and he was like, “I about drove off the side of the road when I heard y’all’s voices on a podcast I’d put on.” So, go check it out. I know he’s talking about Iced Coffee Hour, and I’m like, “Shame on him that he’s not listening to our stuff every week anyway,” but I think it’s, I love getting shout outs from childhood friends and others who might have come across the show. And you guys have been, I’m assuming you watching our live stream have also been the ones writing all the positive comments on the show. Thank you. We I mean it was really cool to kind of see the visit actually turn out as well as it did. And we appreciate that Graham and Jack gave us the opportunity. They reached out to us and said, “Hey, do you want to come on the show?” Like, “Yeah, we’d love to, you know, have access to your 1.3 million subscribers to show what we do here with the Financial Order of Operations.” So, thanks for all the positive comments and thanks for just always supporting us because I think you guys can tell where our heart is is that we really are trying to with the financial order of operations, with the abundance cycle is we want people to be successful with their money. There really is a better way to do money as Bo even started the show today. So use our system, take advantage of all of our free stuff. Go to moneyguy.com/resources. Lean into the free stuff. Maximize yourself and then that of course creates the graduation point of the abundance cycle of becoming a client. We’ll leave the porch light on. I’m your host Brian Preston, Mr. Bo Hanson, Rebie and the rest of the content team. Money Guy out.

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month…

View Resource

How Much Should You Save?

Know how much to save to fund your retirement lifestyle. How much of your income can you replace in retirement?…

View Resource

Are You a Prodigious Accumulator of Wealth?

Find out if you’re a Prodigious Accumulator of Wealth. Is your net worth on-track for retirement? You might be saving…

View Resource

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Subscribe to our free weekly newsletter by entering your email address below.

")